Hiring an unlicensed carpet removal service feels like a bargain until a worker gets injured and you're liable for their medical bills. After thousands of removals, we've seen customers face five-figure injury claims because they didn't verify licensing and insurance. This guide shows you exactly how to protect yourself: what to ask before hiring, how to verify credentials, and what happens when something goes wrong. Because licensing and insurance aren't red tape—they're the difference between a smooth removal and financial liability you can't escape.

TL;DR Quick Answers

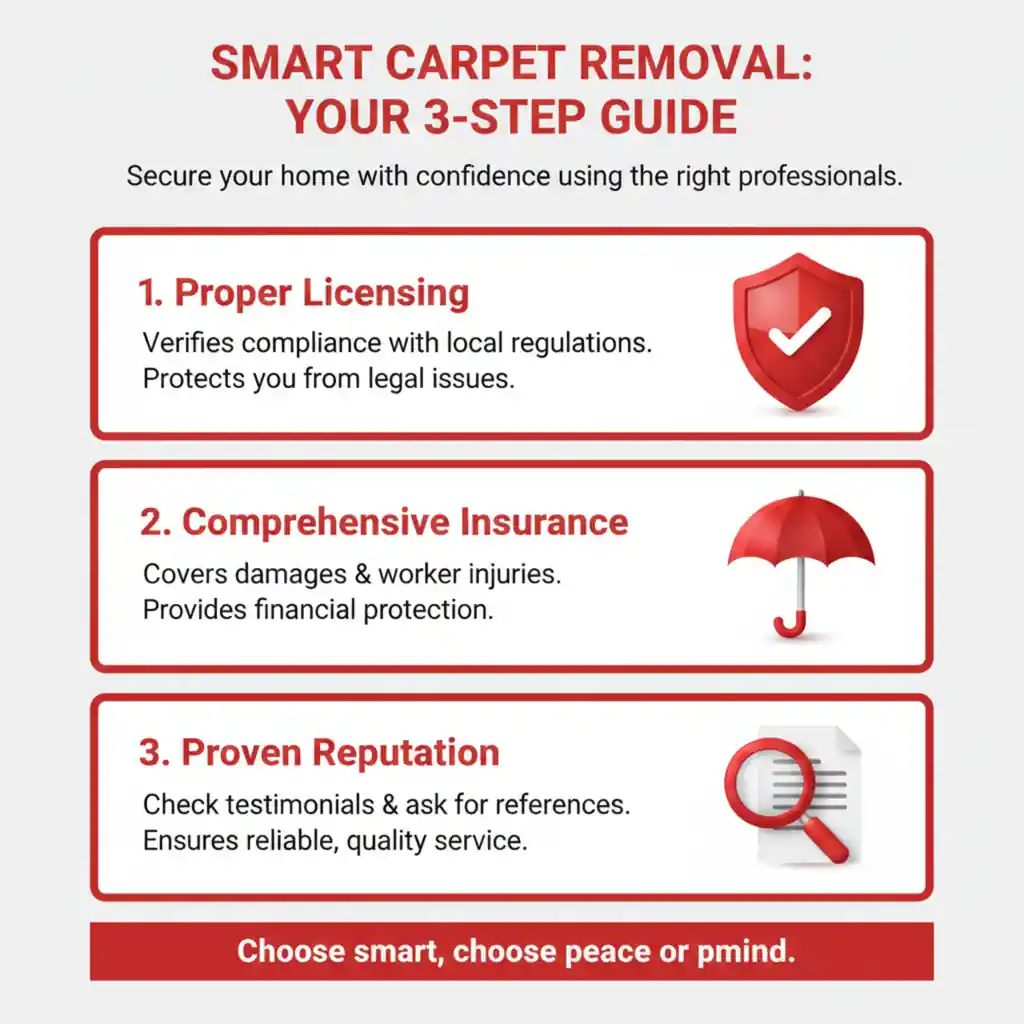

What is a licensed and insured carpet removal service?

A professional carpet removal service that has been verified by your state as meeting safety and regulatory standards, carries workers' compensation insurance for employee injuries, and general liability insurance for property damage. You can verify licensing with your state's Contractor Licensing Board. Asking for proof isn't optional—it's essential protection.

Why should I hire a licensed contractor instead of an unlicensed one?

An unlicensed contractor transfers all liability to you. If an employee gets injured, you pay the medical bills (average $47,316). If property gets damaged, you pay for repairs. If asbestos gets disturbed improperly, you face health liability. A licensed, insured contractor's insurance covers these incidents. The 15-25% price premium protects you from catastrophic financial liability.

How do I verify a contractor's license and insurance?

Call your state's Contractor Licensing Board and provide their license number. Ask for their current Certificate of Insurance and call the insurance company directly to confirm coverage. Don't accept verbal assurances or suspicious-looking certificates. Verification takes 15 minutes and prevents thousands in liability. We do this ourselves before hiring—you should too.

What happens if I hire an unlicensed contractor and someone gets injured?

You become personally liable. No insurance company exists. The injured worker can sue you directly. Medical bills, lost wages, rehabilitation—you pay for all of it. The contractor often disappears once the job is done. We've talked to homeowners who saved $300 by hiring unlicensed and faced $47,000 claims. The math doesn't work.

What questions should I ask a contractor before hiring?

Ask these critical questions:

What is your license number? (Verify it immediately)

Can you provide a current Certificate of Insurance?

What is your workers' comp coverage amount?

Do you inspect the floor after removal?

What is your policy if you find asbestos?

A contractor who hesitates or deflects is disqualified. Legitimate contractors answer all of these without hesitation.

What does professional carpet removal actually include?

Professional removal includes:

Carpet and padding extraction

Tack strip and staple removal

Debris removal from your home

Floor cleanup and inspection

Proper disposal or recycling

Many unlicensed services stop at pulling up carpet. Licensed services do the complete job and inspect for damage, water issues, or mold. You pay more for completeness because it protects you and helps you choose the different types of air purifiers if indoor air issues are found.

Is asking for licensing and insurance documentation excessive?

No. It's baseline protection. A contractor who provides proof of licensing and insurance immediately is operating responsibly. A contractor who hesitates, makes excuses, or refuses is operating outside accountability systems. Your protection should never be considered excessive. Any legitimate business has these credentials ready.

How much more does licensing and insurance cost compared to unlicensed operators?

Licensed contractors typically cost 15-25% more. That premium covers insurance, state licensing, safety training, bonding, and accountability. An unlicensed operator quotes low because they skip all of it. You're not overpaying for licensing—you're underestimating the risk of hiring without it. The $300 savings becomes a $47,000 liability.

Top Takeaways

1. Licensing Isn't Bureaucratic Overhead—It's Your Only Verification Method

A licensed contractor has:

Passed state inspections

Meets safety standards

Carries bonding

Is accountable to regulatory oversight

An unlicensed contractor has none of this.

Verify the license number with your state licensing board. It takes five minutes. Non-negotiable.

2. Workers' Compensation Insurance Costs Average $47,316 Per Claim

When an unlicensed crew member gets injured on your property:

You become personally liable

No insurance exists

You cover everything

Medical bills + lost wages + court costs + legal fees = Your problem.

A licensed, insured contractor's insurance covers it. That $300-400 price difference isn't savings. It's a risk transfer.

3. Verification Takes Minutes But Protects You for Years

Demand and verify before hiring:

State license number (call the licensing board)

Current Certificate of Insurance (call the insurer)

Workers' comp and general liability coverage amounts

References from recent jobs (actually call them)

A contractor who hesitates is disqualified.

4. The Cheapest Quote Usually Hides an Unlicensed Operator

Licensed contractors quote 15-25% higher because they:

Carry insurance

Maintain safety standards

Train crews

Accept accountability

Unlicensed operators skip all of this.

You're not comparing prices. You're comparing risk. Cheap now = catastrophic liability later.

5. Your Personal Liability Is Unlimited If You Hire Unlicensed

Construction injury costs:

Average claim: $47,316

Amputations: $125,058

Head injuries: $90,043

Multiple body parts: $77,614

These are averages. Not the worst case.

When something goes wrong with unlicensed:

No insurance company

No appeals process

Just you, the bills, and potential bankruptcy

Licensing isn't bureaucratic overhead. It's proof that a contractor meets minimum safety standards, has been vetted by the state, and is accountable to regulatory oversight. A licensed carpet removal service has passed inspections, carries bonding, and operates within legal guidelines—which means if something goes wrong, there's a paper trail and an agency you can contact.

We've encountered unlicensed operators who cut corners on safety, skip proper disposal procedures, and disappear when problems arise. Homeowners who hired them had no recourse because there was no official record of the company. Without licensing, you have no protection if the contractor damages your home or a worker gets injured.

An unlicensed contractor might charge 30% less upfront. But when something goes wrong—a worker falls, your subfloor gets damaged, asbestos isn't handled properly—you become the liable party. That $300 savings turns into a $10,000 liability you can't escape.

What Insurance Actually Protects You From

Insurance is your safety net. Professional liability insurance covers property damage the crew causes. Workers' compensation insurance covers injuries to the contractor's employees. Without it, you're on the hook.

Here's the scenario we've seen too many times: An unlicensed contractor is removing carpet. A worker slips and breaks their leg. The contractor has no workers' comp insurance. The injured worker sues you, the homeowner, for medical bills. You're liable for tens of thousands of dollars because the contractor wasn't insured. Your homeowner's policy won't cover it because the injury happened during a professional service.

Legitimate carpet removal services carry both:

General liability insurance (protects against property damage they cause)

Workers' compensation insurance (covers employee injuries)

The small cost of maintaining insurance is built into their quote. Legitimate companies factor it in because they operate responsibly.

How to Verify Licensing Before Hiring

Never take a contractor's word for it. Verification takes five minutes and protects you completely.

Step 1: Find your state's contractor licensing board. Search "[Your State] Contractor Licensing Board" or visit your Secretary of State website. Every state maintains a public database of licensed contractors.

Step 2: Search the contractor's name and license number. The database will show:

Current license status (active or expired)

License type and classification

Disciplinary history

Complaints filed against them

Whether they're bonded

Step 3: Verify the license matches the service. A carpet removal license is specific. If the contractor lists a general handyman license or claims licensing in a different state, that's a red flag.

Step 4: Ask for their license number directly. A legitimate contractor will provide it without hesitation. If they seem evasive or say "it's just a small job, we don't need a license," that's your signal to walk away.

How to Request and Review Insurance Documentation

Insurance verification is straightforward. Ask for it in writing before work begins.

What to request:

Certificate of Insurance showing general liability coverage

Workers' compensation insurance certificate

Coverage amounts (general liability should be minimum $300,000-$1,000,000 depending on your state)

Current policy dates (verify they're not expired)

What to check on the certificates:

Policyholder name matches the contractor's business name

Coverage amounts are adequate

Policy dates are current (not expired)

Your address is listed as the job location

The insurance company is legitimate (verify by calling the insurer directly)

Red flags:

Contractor can't produce certificates

Certificates are expired

Coverage amounts are suspiciously low

They offer to "add you to their policy" verbally without documentation

Don't accept verbal assurance. Get it in writing.

What Happens When Something Goes Wrong

If a licensed, insured contractor causes damage or an injury occurs, there's a clear path to resolution.

Scenario: Worker gets injured A licensed contractor with workers' comp insurance has coverage for the injury. Their insurance pays medical bills and lost wages. You're not liable. The injury is documented with the state, creating accountability.

Scenario: Contractor damages your hardwood floor Their general liability insurance covers the damage. You file a claim, the insurance pays for repairs, and the claim is documented. If disputes arise, you have an insurance company managing resolution.

Scenario: Contractor does shoddy work You have documentation (license number, insurance company) to file a complaint with the state licensing board. The board investigates. The contractor's license is at risk if they violate standards. This creates accountability.

What happens with unlicensed contractors: No insurance claim to file. No licensing board to contact. No documented agreement to enforce. You're left calling the contractor's cell phone (often disconnected) and paying for repairs out of pocket.

Red Flags That Signal an Uninsured or Unlicensed Contractor

Watch for these warning signs:

No business address or only a cell phone number — Legitimate services have a fixed location and verifiable contact info.

Refuses to provide license number or insurance documentation — Any hesitation here is disqualifying.

Quotes significantly lower than other contractors — Often because they're skipping licensing, insurance, and safety protocols.

Offers to bill you directly to "avoid paperwork" — Translation: avoiding documentation and tax reporting. Red flag for unlicensed operation.

Works only on cash payments — Makes it harder to document the job and their legitimacy.

Claims "licensing isn't necessary for small jobs" — False. Licensing requirements don't change based on job size.

Can't provide references or recent project information — Legitimate contractors have satisfied customers they can reference.

Questions to Ask Before Hiring

Ask these questions in writing via email. The answers create a documented record.

What is your license number and state of licensure? (Verify it immediately after they respond)

Can you provide a current Certificate of Insurance? (Get it before scheduling)

What is your workers' compensation insurance coverage amount?

What is your general liability insurance coverage amount?

Can you provide references from jobs completed in the last 30 days? (Call them)

What happens if your crew damages my subfloor or discovers asbestos? (Their answer reveals whether they have protocols in place)

Are you bonded? (Bonding provides additional protection if disputes arise)

Do you have a written contract specifying scope, timeline, and payment terms? (Get it in writing)

A professional contractor answers all of these without hesitation. An unlicensed operator deflects or makes excuses.

The Cost of Cutting Corners

A licensed, insured carpet removal service costs 15-25% more than an unlicensed operation. That premium covers:

State licensing and regulatory compliance

Workers' compensation insurance

General liability insurance

Bonding

Accountability if something goes wrong

That extra cost is protection. When you hire unlicensed, you're not saving money—you're transferring risk to yourself. A single injury claim or property damage incident wipes out any savings and creates liability you can't escape.

Your Checklist Before Hiring

Before any contractor steps foot in your home:

✓ Verify their license with your state's licensing board

✓ Request and review current Certificate of Insurance

✓ Confirm coverage amounts are adequate for your situation

✓ Get three references from recent jobs and call them

✓ Get everything in a written contract (scope, timeline, payment terms)

✓ Verify the contractor's business name matches their license and insurance documentation

✓ Ask how they handle damage or accidents on the job

✓ Get proof of bonding if available in your state

A contractor who checks all these boxes protects you. One who resists or deflects on any of them should be disqualified.

The bottom line:

Licensing and insurance aren't optional add-ons. They're the foundation of professional service. When you hire a licensed, insured contractor, you're not paying extra—you're protecting yourself from liability that could cost tens of thousands of dollars, which can drastically increase your estate cleanout cost if something goes wrong.

Ready to hire a carpet removal service you can trust? Contact Jiffy Junk. We're fully licensed, bonded, and insured. We provide proof of all credentials upfront, carry comprehensive coverage, and stand behind every job. Your protection is our standard.

"Early on, we watched a homeowner get sued by an injured worker because they hired an unlicensed contractor. The contractor disappeared, and the homeowner—who thought they saved $400—ended up paying $15,000 in medical bills because the contractor had no insurance. That case changed how we operate. Now, licensing and insurance aren't just compliance requirements for us—they're foundational commitments we verify every single time. When a customer hires Jiffy Junk, they know exactly who they're hiring, what protections they have, and who to contact if something goes wrong. We've made it our standard because we've seen what happens when contractors cut corners. The $300 a homeowner saves by hiring unlicensed isn't savings—it's deferred liability."

Essential Resources

Verify Contractor Licensing Instantly: Your State's Contractor Licensing Board

We check this first on every job we do. It takes five minutes and reveals everything: active license status, what classification they hold, any disciplinary history, and whether they're bonded. This is your real protection. When we hire our team members, we verify against this same database. If a contractor won't give you their license number or seems evasive about it, that's your first red flag.

Track Complaint History and Resolution: Better Business Bureau (BBB) — Contractor Search

We've learned that one bad review is normal—any service gets those. But three complaints about the same issue? That's a pattern. The BBB shows you patterns. We monitor our own BBB profile constantly because it reflects our commitment to solving problems. When you search a contractor here, look for whether they responded to complaints and how they resolved them. That tells you if they stand behind their work or disappear when issues arise.

Know Your Legal Protections: Federal Trade Commission: Hiring Home Contractors Safely

https://consumer.ftc.gov/articles/0211-hiring-home-contractors

The FTC exists because too many homeowners get burned without knowing their rights. We've seen customers who didn't get written contracts discover mid-job that the scope changed and the price doubled. The FTC explains exactly what you're legally entitled to demand before work begins. Read this before you call anyone. It changes how you negotiate.

Understand Professional Safety Standards: OSHA Occupational Safety Standards

Know what you're looking for. OSHA defines how professional flooring removal should be handled safely and how workers should be protected. When you understand the standard, you can spot contractors cutting corners. We train our crews to OSHA standards because one injury—to them or on your property—creates liability nobody wants.

Verify Insurance Company Legitimacy: National Association of Insurance Commissioners (NAIC) — Insurance Verification

A contractor hands you an insurance certificate that looks official. But is the company actually licensed? NAIC lets you verify. We've heard stories of contractors showing fake insurance certificates. Verify the insurance company is real. Call them directly. Confirm the policy exists. Don't take a piece of paper at face value—especially one that protects you financially.

File Complaints and Protect Yourself: Your State Attorney General's Office — Consumer Protection Division

If a contractor damages your home or a worker gets injured and they're uninsured, your state attorney general's office has enforcement tools. We recommend every customer know who to contact and how to file a complaint. It creates accountability. Contractors know their licensing and behavior are monitored—and that's exactly the pressure that keeps the industry honest.

Verify Industry Standards and Certifications: Professional Junk Removal and Hauling Association (JRHA) or Regional Associations

Industry associations matter because membership requires meeting standards. We're members of professional associations in every market we serve. It means we're accountable to standards beyond just state licensing. When you hire someone who's part of these associations, you're hiring someone who voluntarily agreed to follow a higher code. That distinction matters.

These essential resources are critical for a garage cleanout because they help you confirm the contractor is licensed, insured, and safety-compliant before they handle heavy debris, hazardous materials, or hidden damage.

Supporting Statistics

The numbers back up what we've learned through thousands of residential removals: unlicensed contractors create financial liability homeowners never anticipate.

Construction Industry Injury Rates Are Higher Than You Think

The data: Construction recorded 2.3 nonfatal occupational injuries per 100 full-time workers in 2023 (U.S. Bureau of Labor Statistics).

What we've seen: That 2.3% statistic becomes 100% your personal liability if the contractor lacks workers' compensation insurance.

The scenario: A crew member gets injured on your property. No insurance. The contractor disappears. You're liable for:

Medical bills

Lost wages

Potential legal action

Court costs

Real example: We've encountered homeowners who thought they saved $300-400 by hiring unlicensed. Then an injury happened. Five-figure liability. Personal bankruptcy risk.

Source: https://www.bls.gov/iag/tgs/iag23.htm

Workers' Compensation Claims Cost an Average of $47,316 Per Claim

The number: Average workers' compensation claim cost (2022-2023): $47,316

According to the National Council on Compensation Insurance (NCCI)

What it means: That's the baseline. Not the worst case. Just average.

Costlier injuries include:

Amputations: $125,058 average

Head/central nervous system injuries: $90,043 average

Multiple body part injuries: $77,614 average

The trap homeowners fall into:

Hire unlicensed contractor to save money

Crew member gets injured

No workers' comp insurance exists

Homeowner pays entire claim out of pocket

Financial devastation

Source: https://injuryfacts.nsc.org/work/costs/workers-compensation-costs/

Construction Injuries Cost the Industry Billions Annually

The trend: Fatal construction injuries increased 39.8% from 2011 to 2022 (CPWR).

The risk landscape:

Construction: 5% of U.S. employment

Construction: 20% of all workplace fatalities

Specialty trade contracting: 60.8% of construction fatalities (2011-2022)

Carpet and flooring removal falls into specialty trade contracting—the highest-risk category.

Why these statistics exist: Someone cut corners. Someone operated without oversight. Someone had no accountability.

Our approach: Licensed operation. Insured operations. Trained crews. Accountability. Safety standards. Documentation. None of this happens without licensing and insurance.

Source: https://www.cpwr.com/wp-content/uploads/DataBulletin-July2024.pdf (CPWR Construction Fatality Data)

What these statistics mean for your carpet removal project:

A licensed, insured contractor's insurance costs 15-25% more upfront. That premium protects you from:

$47,000+ average worker injury claim

Legal costs

Property damage claims

Lawsuits you can't anticipate

Personal financial liability

The choice:

Save $300-400 now and risk $47,000+ later?

Or hire licensed and insured and sleep at night?

When you hire Jiffy Junk, you're not paying extra for licensing and insurance. You're buying protection from becoming part of these statistics.

Final Thought

After thousands of carpet removals, we've developed a strong opinion: the unlicensed contractor problem isn't just about bad operators. It's about homeowners who don't verify credentials before hiring.

What we've seen:

A homeowner calls three contractors for quotes:

Contractor A: Licensed, insured. Quote: $1,500

Contractor B: Unlicensed. Quote: $1,000

Contractor C: Unlicensed. Quote: $1,100

The homeowner picks the cheapest option. Six months later, a crew member gets injured.

Result:

Can't reach the contractor

No insurance to cover the claim

Personal liability: $47,000 workers' compensation claim

That $400 savings became six-figure liability

The uncomfortable truth:

Licensing and insurance aren't optional. They're foundational safety mechanisms that exist because something went wrong before.

When you hire unlicensed, you're not saving money. You're transferring risk to yourself.

What unlicensed contractors do:

Cut corners on safety

Skip disposal standards

Avoid training requirements

Don't carry insurance

Disappear when problems arise

When something goes wrong, you become the liable party.

What licensing and insurance actually mean:

Licensing = State inspection, safety standards compliance, bonding, regulatory accountability

Insurance = Coverage when injuries happen, property gets damaged, or incidents occur

The difference when something goes wrong:

Licensed, insured contractor: Insurance covers the claim

Unlicensed contractor: You cover the claim personally

Why the industry standard is broken:

Too many homeowners:

Compare quotes by price only

Don't ask for license numbers

Don't request insurance certificates

Don't verify anything

Act shocked when something goes wrong

Our commitment:

We operate licensed and insured in every market we serve. Not because it's trendy. Because it's the only responsible way.

What we do:

Train crews to OSHA standards

Maintain equipment properly

Provide worker protection

Provide client protection

Document everything

Stand behind every job

Accept accountability

What homeowners should demand:

License number verified with state licensing board (before work begins)

Certificate of Insurance showing workers' comp and general liability

Current insurance policy dates (not expired)

Written estimate itemizing scope, timeline, payment terms

References from recent jobs (call them)

A contractor who hesitates on any of these should be disqualified immediately.

The reality:

When you hire unlicensed to save $400, you're accepting risk transfer. You're saying you'll be personally liable if something goes wrong.

That's not negotiation. That's financial recklessness.

Choose a contractor that operates properly:

✓ Licensed and verified with state

✓ Fully insured with current certificates

✓ Bonded where available

✓ Provides written estimate and contract

✓ Stands behind their work

✓ Maintains documentation

✓ Accepts accountability

That contractor costs more upfront. That contractor protects you financially. That contractor is worth every penny.

Ready to hire a carpet removal service that operates with integrity?

Contact Jiffy Junk.

We're licensed, bonded, and fully insured in every market. We verify and document everything. We provide proof of all credentials upfront. We train crews to professional standards. We've seen what happens when contractors cut corners.

Your protection is our standard.

FAQ on Carpet Removal Service

Q: How do I verify if a carpet removal contractor is actually licensed?

A: Search your state's Contractor Licensing Board website.

Enter the contractor's name and license number.

Results show:

License status (active or expired)

Classification

Disciplinary history

Bonding information

It takes five minutes. Free. Non-negotiable.

A contractor who hesitates to provide a license number is telling you something. Legitimate contractors provide it immediately.

Q: What insurance should a carpet removal contractor have, and how do I verify it?

A: They must carry:

Workers' compensation insurance (covers employee injuries)

General liability insurance (covers property damage)

What to verify:

Request Certificate of Insurance in writing

Check policy dates (must be current, not expired)

Verify coverage amounts ($300,000-$1,000,000 minimum general liability)

Call the insurance company directly to confirm the policy exists

Never accept verbal assurances. Don't trust certificates that look suspicious. Verify independently.

Q: What happens if a contractor's employee gets injured at my house and they don't have insurance?

A: You become personally liable.

You pay for:

Medical bills

Lost wages

Rehabilitation costs

Legal fees

Average workers' compensation claim: $47,316 Amputation claims: $125,058 average Head injury claims: $90,043 average

If the contractor disappears (they usually do):

No insurance company to contact

No appeals process

You hire a lawyer hoping to recover costs

Verify insurance before work begins. This isn't paranoia. This is self-defense.

Q: Why does a licensed, insured contractor cost 15-25% more than an unlicensed operator?

A: The premium covers:

Workers' compensation insurance

General liability insurance

State bonding

State licensing fees

Safety training programs

Equipment maintenance

Documentation systems

Accountability infrastructure

An unlicensed contractor quotes low because they skip all of this.

They're not negotiating. They're transferring risk to you.

The price difference is protection you're buying, not markup you're overpaying.

Q: What red flags should I watch for when a contractor refuses to provide licensing or insurance information?

A: Disqualifying red flags:

Can't provide license number

Says licensing isn't necessary

Refuses Certificate of Insurance in writing

Only accepts cash payment

Demands full payment upfront

No business address—only cell phone

Can't provide recent job references

Quotes suspiciously low compared to others

Refuses written estimate or contract

Pressures you for immediate decision

One red flag = disqualified.

These contractors operate outside the system intentionally. Don't become liable for their negligence.